I’ve read a bunch about the subject and will probably do something like a fixed-percentage variable spending scheme, like Vanguard proposes. But I’m curious what people are actually doing in real life. Is anyone out there managing their retirement finances, and if so, how did you figure your SWR?

Edit: So here’s the system I’m thinking of using. The numbers are just an example.

First determine my SWR, which is what I’m having a problem with, but let’s say it’s $60,000/year. This comes out to $5000/month.

Initially, I’d fill up my bank account with $5000, and treat it like an allowance. Each month, I’d just top my account back up to $5000. On most months, I wouldn’t have spent the whole thing anyway. The next year, I’d make an adjustment for inflation, and that would be my new monthly allowance. Repeat until I’m dead.

Thoughts?

I’m planning to do the same thing as you are. Hopefully only 4 years out now…

I’m earmarking 4% SWR with variance, but in reality the salary I’m planning to pay myself in retirement is more than 2x my current expenses, so I guess that makes my literal SWR closer to 2%. 🤷

More or less, I’m playing it by ear. Idk if I will even stop working in 5 years (my timeline) - depends on what the market is doing and how jaded I feel about my job. Riding the snowball for just a couple more years of work can net me a lot more money to retire with, but there’s really no logical stopping point if all you think about is how much money you’re going to make next year.

This is not answering your question (I can’t argue for my current SWR, it’s the trinity study minus a random fudge factor), but I’ve implemented an idea that I think others would benefit from.

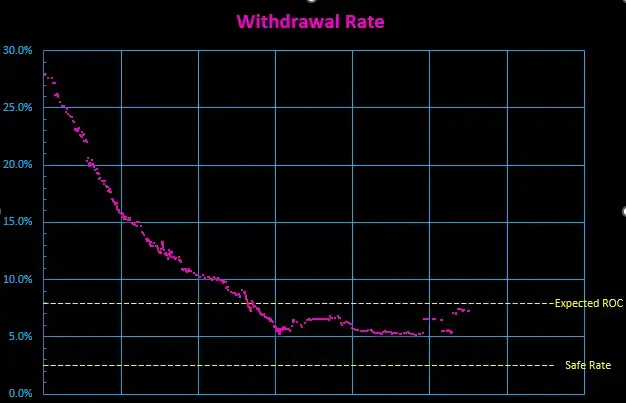

I’ve been tracking my current withdrawal rate through time, based on my periodic calculation of baseline expenses. I suppose I could use actual expenses, but that’s remarkably volatile, so instead I take the 6 month average of recurring costs.

The benefit is a nice time series graph I can watch. I can plot a horizontal line for my current expected return on capital, and another for my safe withdrawal rate.

The net result is a lot of information condensed nicely. You can see at a glance if you’re trending towards safety, or away from it.

For planning I used detailed monte carlo model for planning that included expected age varying costs. Like SWR but not constant spending. Played with simpler models too.

For execution between now and age 70 pensions, SS, and an annuity will phase in to cover all of our basic inflation escalated expenses. Portfolio will only be for discretionary stuff. I also have a spreadsheet that I used as kind of a control chart to track spending, assets, and spending capability over time.

I might try to do something more sophisticated in the future … Like a monte carlio model with partial variable spending and taking CAPE into account but for now that is beyond what I do.

Personally I think the constant inflation escalated payout people talk about is not that useful during the execution phase. Handy during planning though.

deleted by creator